Tuesday, February 24, 2026

The Next Wave of Data Center Real Estate: Inside Amazon, Oracle, and Google’s Massive Builds

The global data center real estate market is entering a new phase of expansion — one defined not just by demand, but by scale, speed, and strategic land control.

Across North America, Europe, and emerging growth markets, hyperscalers like Amazon Web Services (AWS), Google, and Oracle are actively developing new data center campuses at unprecedented levels. These aren’t speculative builds. They are carefully staged, power-secured, multi-phase real estate plays designed to support AI workloads, cloud expansion, and long-term digital infrastructure dominance.

For investors, developers, and enterprise tenants, projects currently under construction reveal where infrastructure capital is flowing — and where tomorrow’s capacity will be concentrated.

Hyperscalers Are Securing Land Before They Announce Capacity

One of the most important shifts in data center real estate is timing. Hyperscalers are acquiring and entitling land years before vertical construction becomes visible.

Instead of reacting to demand, companies like Amazon, Google, and Oracle are:

- Locking up large land parcels near power corridors

- Securing long-term utility agreements

- Pre-negotiating water and sustainability approvals

- Designing phased campuses expandable over 10–20 years

This land-banking strategy is especially visible in markets like:

- Northern Virginia

- Central Ohio

- Dallas-Fort Worth

- Phoenix

- Atlanta

- Indiana and Iowa

- Spain and parts of Northern Europe

In many cases, the real estate transaction happens quietly. Construction follows once power allocations are guaranteed.

For data center real estate professionals, this signals a fundamental truth: control of land with power access is now more valuable than speculative shell development.

Amazon’s Ongoing Global Expansion

Amazon Web Services continues to be one of the most aggressive data center developers globally.

Rather than building single facilities, AWS typically develops multi-building campuses designed for long-term regional dominance. Under-construction projects often include:

- Multiple availability zones within a metro

- Dedicated substations

- High-density AI-ready halls

- Significant fiber interconnectivity

AWS projects are frequently phased, with initial megawatts delivered quickly and additional capacity rolled out as demand ramps.

From a real estate perspective, Amazon prioritizes:

- Proximity to reliable utility infrastructure

- Favorable tax and incentive environments

- Large, scalable land footprints

- Political and regulatory stability

These factors are shaping new development corridors beyond traditional Tier I markets.

Google’s AI-Driven Construction Pipeline

Google’s recent construction strategy reflects the accelerating infrastructure needs of artificial intelligence and machine learning workloads.

New Google data center developments increasingly feature:

- Higher power density designs

- Advanced cooling systems

- Long-term renewable energy commitments

- Strategic placement near fiber backbones

Google often partners closely with utilities to co-develop grid expansions. In some regions, data center construction is occurring alongside new renewable generation projects.

For data center real estate markets, this creates a secondary effect: once Google commits to a region, surrounding land values and infrastructure investment tend to rise.

Construction activity also signals confidence in long-term digital growth, which can catalyze additional colocation and wholesale development nearby.

Oracle’s Cloud Infrastructure Acceleration

Oracle has significantly accelerated its cloud footprint in recent years.

Unlike traditional hyperscale rollouts, Oracle’s expansion strategy often targets:

- Underserved secondary markets

- International growth regions

- Enterprise-driven demand corridors

New Oracle data center projects under construction frequently emphasize:

- Rapid deployment timelines

- Strategic enterprise proximity

- Sovereign cloud considerations

This creates opportunities in markets that historically were not viewed as hyperscale hubs.

From a data center real estate standpoint, Oracle’s expansion highlights a broader shift: hyperscale construction is no longer limited to a handful of gateway metros.

Construction Trends Defining 2026 and Beyond

Looking across Amazon, Google, and Oracle builds, several clear development patterns are emerging.

1. Phased Campus Development

Instead of single-building projects, developers are planning campuses that can scale from 50 MW to several hundred megawatts over time.

Initial phases are designed for rapid delivery, while long-term infrastructure (substations, water systems, transmission upgrades) supports expansion.

2. Power-First Site Selection

Power availability has overtaken fiber proximity as the primary site selection driver.

Markets with available grid capacity are seeing new construction announcements — even if they were previously considered secondary or tertiary markets.

3. AI-Ready Infrastructure

New builds increasingly assume higher rack densities.

Design elements now commonly include:

- Liquid cooling readiness

- Larger electrical rooms

- Reinforced structural capacity

- Expanded generator yards

Real estate parcels must accommodate these expanded infrastructure footprints.

4. Speed to Market

Hyperscalers are compressing development timelines wherever possible.

Pre-fabricated components, modular electrical systems, and standardized designs are reducing build cycles.

The faster a facility comes online, the faster revenue-generating workloads can deploy.

What This Means for Data Center Real Estate

For investors and developers, projects under construction offer a forward-looking demand indicator.

When Amazon, Google, or Oracle commits capital to a region, it typically signals:

- Long-term cloud growth expectations

- Increased fiber and connectivity investment

- Strengthened local infrastructure

- Secondary demand from enterprises and service providers

In many cases, hyperscale construction de-risks surrounding real estate for:

- Wholesale colocation developers

- Powered shell investors

- Industrial land assemblers

- Infrastructure funds

Additionally, competition for power has reshaped valuation models. Sites with pre-secured utility capacity now command significant premiums.

Emerging Development Markets to Watch

While Northern Virginia remains active, new construction pipelines are expanding into:

- Midwest markets with grid availability

- Southern U.S. states offering land and incentives

- Select European corridors with renewable access

- Parts of Latin America seeing cloud investment

- Asia-Pacific regions focused on sovereign capacity

Hyperscale construction is no longer confined to legacy hubs. It is increasingly shaped by grid feasibility, policy alignment, and renewable integration.

The Strategic Shift From Leasing to Owning Infrastructure

Another notable trend: hyperscalers continue balancing leasing with owned development.

While wholesale colocation remains critical for speed and flexibility, ownership provides:

- Greater long-term cost control

- Customized AI-ready infrastructure

- Strategic grid integration

- Campus-level scalability

This hybrid strategy is influencing the broader data center real estate ecosystem. Developers must now anticipate whether hyperscale tenants intend to lease or build in a given market.

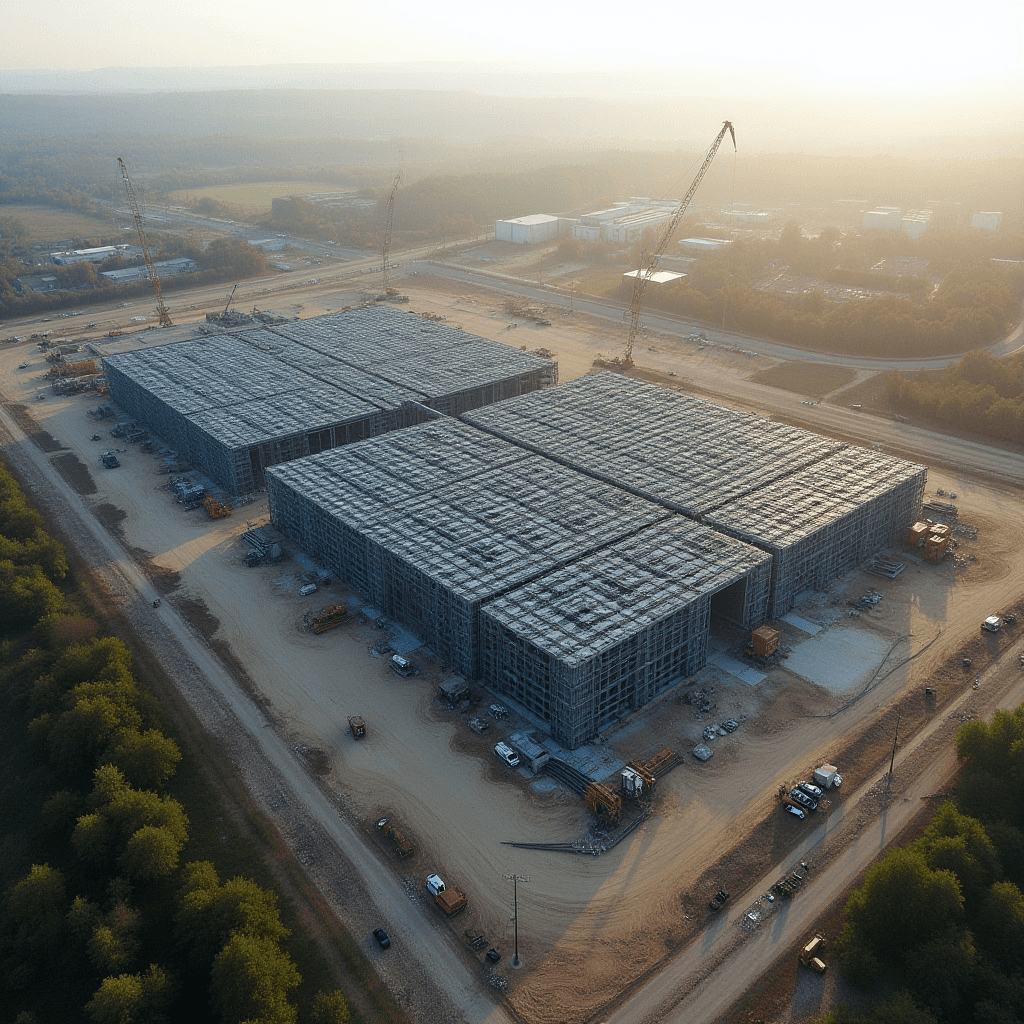

Reading Construction as a Market Signal

New data center projects under construction are more than infrastructure milestones. They are signals of capital conviction.

Where cranes rise, long-term digital demand is already underwritten.

For data center real estate professionals, the key questions become:

- Where is power still obtainable?

- Which markets offer scalable land?

- How quickly can infrastructure be delivered?

- Which hyperscalers are expanding aggressively in specific regions?

As Amazon, Google, and Oracle continue building across global markets, their development footprints are quietly redrawing the map of digital infrastructure.

The next phase of data center growth will be defined not just by demand — but by who controls the land, the power, and the construction pipeline.